The Collaboration Code: Why Partnerships Are the Real Engine of Fintech Adoption in Emerging Markets

Insights

Back to blog

Florence Githinji

2025-09-30

Insights

On this page

In markets where trust is paramount and infrastructure is developing, going it alone is a recipe for failure. True, sustainable growth is a team sport.

Share this article

For the last several years, the story about fintech in emerging markets has been about disruption: the lone innovator developing a "killer app" that will independently bank the unbanked. As a partnerships director who has been working and living in Africa for many years, I can assure you that this is a dangerously simplistic fantasy. The idea that a single company can build, distribute, and scale a financial service from the ground up is inefficient and fundamentally misunderstands the reality of how these markets operate.

The real key to unlocking the immense potential of digital finance isn’t a single product, but a collaborative ecosystem. The “build it and they will come” model fails because it ignores the foundational pillars of commerce in these regions: trust, existing networks, and last-mile accessibility.

Consider the landscape. Across Sub-Saharan Africa, hundreds of millions of people remain unbanked or underbanked. The World Bank’s Global Findex 2021 database notes that while mobile money is booming, formal bank account ownership still lags. The challenge isn’t a lack of desire for financial services; it’s a gap in trusted and accessible infrastructure.

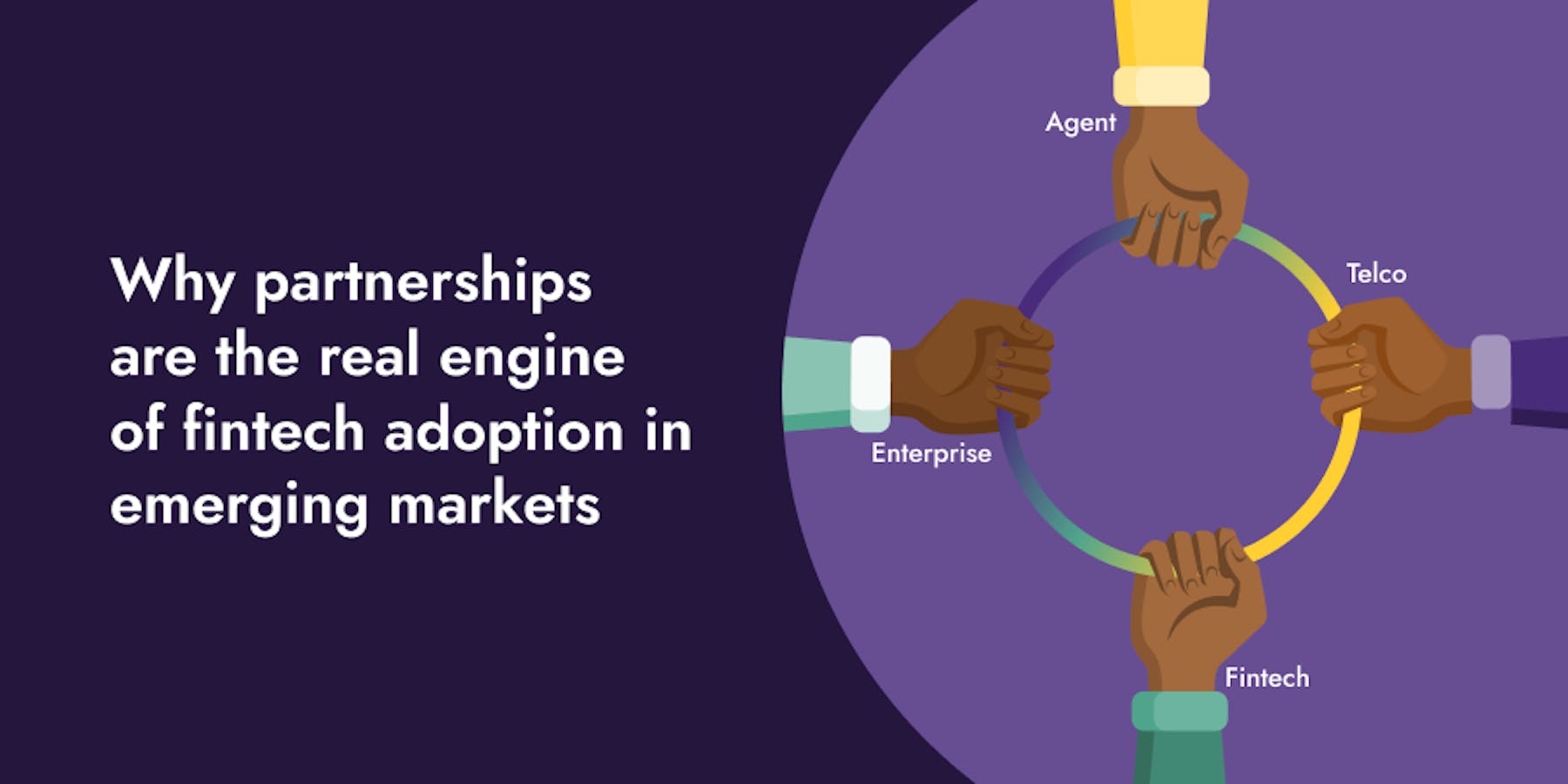

That is where partnerships change everything. Rather than trying to reinvent the wheel, some smart fintechs are plugging into the existing commercial and social fabric of the continent.

In essence, they are doing a series of strategic handshakes:

Fintechs + Telcos: Telcos or mobile network operators have what every startup wants - a massive and pre-existing user base and some form of established trust. Fintechs using telcos' mobile money platforms can immediately solve payment and distribution problems and be able to provide savings, micro-loans, insurance, etc., via the customer touchpoints they already seamlessly use every day.

Fintechs + Agent Networks: There is no substitute for the human touchpoint in a cash economy. The human agents that provide cash-in/cash-out services will always be the necessary link between the digital and the physical worlds. A fintech company may have the best app in the world, but if it does not include a reliable agent network that can convert digital value back to cash, the uptake will be limited.

Fintechs + Other Fintechs: Even competitors can collaborate. By working together to build shared infrastructure, such as KYC (Know Your Customer) protocols or payment gateways, companies can reduce overall costs and provide a better experience to the end-user, ultimately growing the entire market.

We see this everywhere. Take Yellow Card, Africa's first licensed Stablecoin payments orchestrator, empowering businesses across emerging markets with international payments, treasury management, and USD liquidity. Their real genius isn't just in what they built, but how they built it. They don’t have to build a new payment system and process in each country. They directly integrate with partners that their customers already rely on and trust, allowing them to take all of the low-friction on-ramps and off-ramps for crypto using local currencies, eliminating a lot of the friction and leading to faster growth.

This isn’t unique to finance. The e-commerce giant Jumia couldn't have scaled without building an ecosystem. They had to create JumiaPay for payments and a vast network of logistics partners and pickup stations to solve the last-mile delivery problem. Their growth wasn't just about selling goods online; it was about building the collaborative infrastructure to make it possible.

The future of fintech in emerging markets will not be defined by a single winner. It will be shaped by a web of interconnected services—a super-grid of companies, each specializing in one part of the value chain and partnering to deliver a complete, trusted solution. For any company looking to succeed here, the first question shouldn't be, "What can we build?" It should be, "Who can we build it with?"

Disclaimer: This article is for information purposes only and should not be construed as legal, tax, investment or financial advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement or offer by Yellow Card to buy or sell any digital asset. There is risk involved in investing or transacting in digital assets, please seek professional advice if you require one. We do not assume any responsibility or liability for any loss or damage you may incur dealing with digital assets. For more information on Digital Asset Risk Disclosure please see - Risk Disclosure.

Share this article